In management audit a team with a mix of members who are accountants and non-accountants will produce a desirable combination of specialists and will offer a cross fertilization of ideas from different. A description of the form and content of the specialists findings that would allow the CPA to use the findings 3.

Forbidden Jutsu Mas Additional Notes Forbidden Jutsu Mas Compiled By Monkey D Luffy If A Studocu

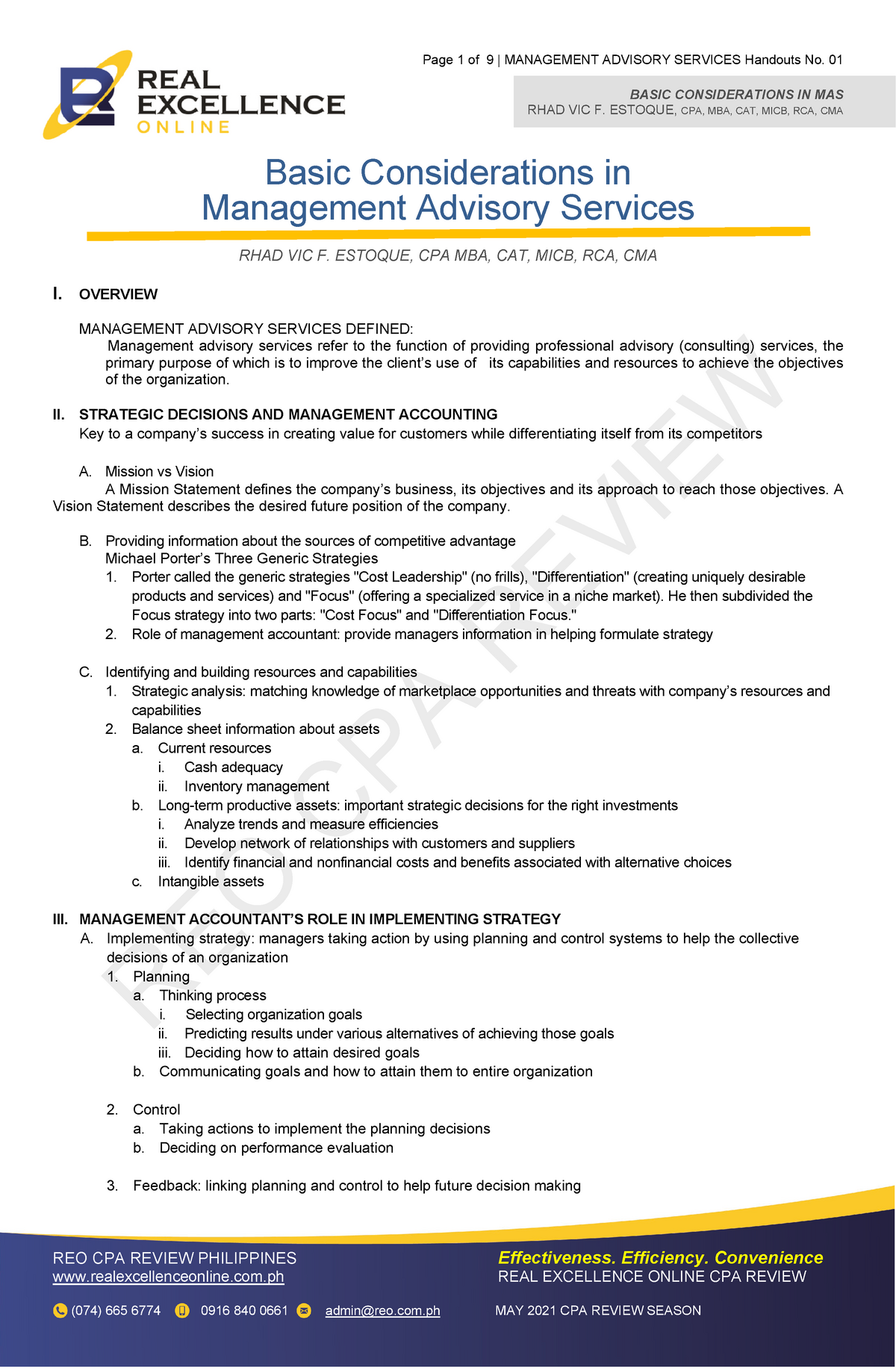

Mission Vision Statement.

The primary source of mas engagements of the cpa. He audits the financial statements of a subsidiary of the prospective client. The engagement of third-party professional services as follows. As of November 2020 186 communities in Massachusetts have adopted the CPA 53 of.

Sl au s 210 presentation trail upload. Constitute advice and assistance b. The manual is for the exclusive use of the CISM Team immediately after a major crisis event in the CBSA workplace which.

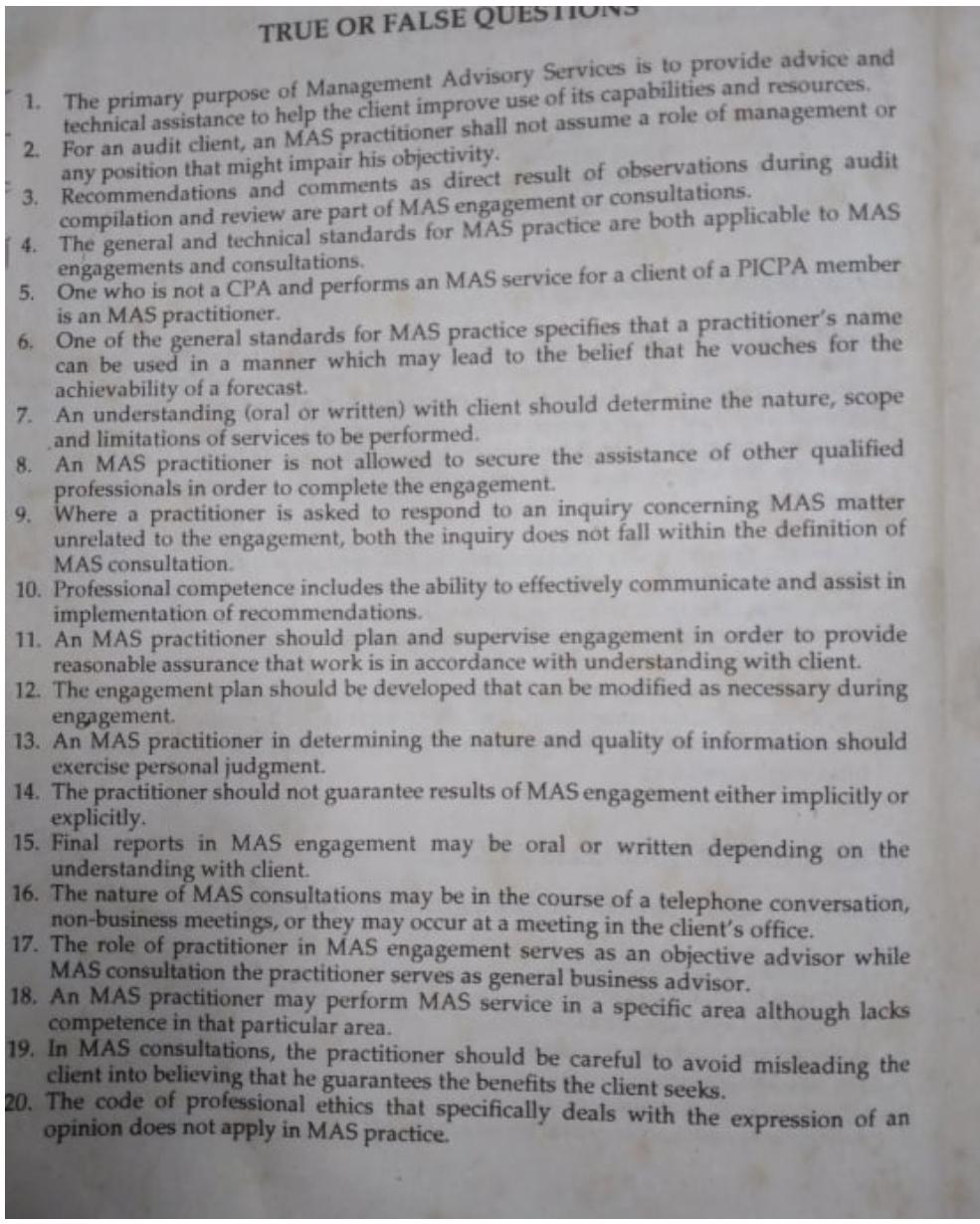

During the tax return preparation process we will make an effort to answer reasonable questions and alert you of potential opportunities. Final reports to a client may be written or oral depending on factors such as The understanding with the client. Another example of an ethical requirement of the Code requires a CPA to be competent in the work he does such as knowing when an engagement is beyond his area of expertise a situatiion when it becomes irresponsible to provide the services.

Protect the working papers from being subpoenaed. His recommendations are to be subjected to a review by the client. The appropriateness of using the specialists work for the intended purpose f.

A CPA is primarily responsible for a clients footnotes in an annual report filed with the SEC. Marketing is an area which is beyond the scope of MAS by CPAs. 2134088700 Sacramento Walnut Creek Century City September 3 2015 Newport Beach To the Honorable Mayor and Members of the.

CPA is funded annually through a combination of two sources a local property tax. A CPA should reject an MAS engagement if a. 2 MAS Engagements states.

While non public companies and non-profit organizations are not required to rotate audit firms or audit engagement partners they need to think about the quality of their audits. The provider in or outside the United States then uploads all scanned documents and relevant tax files to a US. Surcharge 1 to 3 and a yearly distribution from.

Counseling management in its analysis planning organizing operating and controlling functions. The proposed engagement is not accounting related. Unlike audit and attestation services that are.

Evaluating the engagement and post-engagement follow-up I. It is written communication between the CPA and the client setting forth the terms. All consumers are well-informed and receive quality accounting services from licensees they can trust.

For developments of any size that are owned by non-profit organizations or public agencies the cost certification may be completed without the engagement of a CPA. Consulting art Management consulting Full scope engagement Special study engagement Integrity Analytical approach and process Engagement program Competence in professional work Post-engagement follow up Objectivity Code of Professional Ethics Accountancy Law Competence in performing MAS. To protect consumers by ensuring only qualified licensees practice public accountancy in accordance with established professional standards.

The Code provides more detail about when a CPA is responsible for removing herself from the engagement. A CPA firms primary purpose of performing MAS services is to enable the staff members to acquire the necessary continuing education in all areas of business. Certified Public Accountant d.

In a compilation engagement the outside accountant takes the data provided by the client and converts it into financial statements and issues a report on their letterhead. Los Angeles 711 SFigueroa Street Suite 2500 Los Angeles CA 90017 Certified Public Accountants. A CPA firm staff member scans client documents including W-2s 1099s and K-1s into a pdf file saved in the network then sends along the prior-year tax file to the outsource provider.

Negotiating the engagement Proposal letter It is an advisable first step in most MAS engagement. We want you to understand your tax returns. AT-5904 Page 9 of 10 d.

Perform additional procedures if there is a material. The municipalities in Massachusetts. Compiled financial statements represent the most basic level of service that is offered by a licensed CPA with respect to financial statements.

MAS engagement are often closely linked to CPA services in the areas of auditing tax and accounting and may involve activities such as Introducing new ideas concepts and methods to management. Match the following terms with the statements given below. The rationale for this rule is to a.

Engagement of Certified Public Accountants. An attest engagement is one in which a practitioner is engaged to issue or does issue an examination a review or an agreed-upon procedures report on subject matter or an assertion about the subject matter that is the. Unlike in external auditing a CPAs fee for rendering MAS is based on size capitalization or earnings of the client company.

Mas Business. In these cases the Owner. CISM Mass Event Response Plan Introduction and Objective This manual will provide the Mass Event emergency operating procedures and guidelines for the CBSA Pacific Region Critical Incident Stress Management CISM Program.

Click to see full answer. MAS financial ratio analysis engagements may be suggested either by a client or by a practitioner. First a little background on PCAOB audit firm and audit partner rotation and then some information on how non-profits can help ensure a sound audit.

Audits are only designed to test the validity of the financial statements and that only. Documentation is not as essential in an MAS engagement as it is in an audit engagement. In general tax planning and advising are not included with the tax preparation fees.

The current engagement and those used in the preceding engagement e. In performing MAS engagements CPAs should not take any positions that might a. When a CPA in the practice of public accounting performs an attest engagement the engagement is subject to the attestation standards.

Communication of MAS engagement results1 As Statement on Standards for Management Advisory Services No. Very often these engagements result from MAS consultations in which a practitioner recognizes that further analysis or study is needed to achieve the clients objectives. Sources of Financing It provides a study of the.

Provide the basis for excluding admission of the working papers as evidence because of the privileged communication rule. Working papers prepared by a CPA in connection with an audit engagement are owned by the CPA subject to certain limitations. The degree to which the engagement results are provided to the client.

The scope of all engagements will be detailed in the engagement letter. Under an assurance engagement CPAs can provide a variety of services ranging from information systems security reviews to customer satisfaction surveys. Good sources of soluble fibre include fruits vegetables oat bran barley seed husks flaxseed psyllium dried beans lentils peas soy milk and soy products.

Solved True Or False Questions 1 The Primary Purpose Of Chegg Com

Tidak ada komentar